When I started my business journey, I initially sought to find the secret to business success. I suspected there was a secret because only a handful of people experienced success while the majority of people found failure. Additionally of those that found success there were always those serial entrepreneurs that seemed to find one success after another. There was also a ton of examples of people failing at business. Why such a disparity?

The nature of the secret I assumed was a tactical or methodical difference. If I could figure that out I could adopt the methods into my own businesses and live happily ever after. Sorry to say it is not that simple. The difference is more in line with how entrepreneurs think about and address their problems and relationships with people. I hate that this is true. I hate it because it means the answer I was looking for is not something that can be easily defined or discussed.

Take a hall of fame sports star for example. One can’t pin point the things they do habitually that allowed them to make it to the hall of fame. They made it to the hall of fame because of who they are and how they approached their game. The unique reality and un-assessable truth is that they brought a piece of humanity to the table that few others have. Fundamentally they thought about their craft in a unique way.

The reason there are few successful serial entrepreneurs is because there are few people that focus on business and life in the way these people do.

The Dark Side Of The Focused Individual.

Before going into all the “amazing” things these business superheroes can do I would like to discuss the dark side. I have come to believe that how some entrepreneurs approach life and business is something I never want to recreate in my own life. For some serial entrepreneurs their identity is 100% tied to their commercial success. They are one dimensional with their only dimension being business success. That is great if the only thing in life is business but for most of us this will not be the case. For me a well-balanced life is much more important than a having only a commercially successful life.

I discussed how entrepreneurs think in my piece: How to Become an Entrepreneur but I didn’t extrapolate my thoughts to their full conclusions. When entrepreneurs are young they are often misled by the pursuit of profit. While it is true that the goal of a business is to make money now and in the future (thank you Eli Goldratt) the goal of life is not. If the goal of a business is to make money perhaps we should ask; what is the purpose of a money making business? The answer to this will be different for everyone.

I have been really challenged lately with how my time is spent. In his book Hero on a Mission: A Path to a Meaningful Life Donald Miller discusses a technique in which you write your own eulogy. Wow, what a mind bender. The idea isn’t his, Stephen Covey the author of The 7 Habits of Highly Effective People also suggests the exercise. In doing so you begin to see how finite the time we have is and what really matters. Children have forever, teenagers have forever, but a young aspiring entrepreneur may only have a decade or two. What is it you want to do with the handful of years you have left?

How Buying A Machine Shop Changed My Perspective

When I bought a machine shop, I achieved something I thought would never happen in my life time. All the equipment anyone could ask for and the ability to make anything was at my fingertips yet it didn’t take long for my “why” to change. I love manufacturing and making physical goods, solving interesting problems, and establishing sustainable solutions. I very much dislike exchanging time for money. A one to one exchange of time for money is no different than what occurs with a W2 income. It took a handful of breakeven projects for me to refine our approach to the market space. The funny thing was I was the reason we weren’t making money. I was so excited to land jobs that I landed jobs I should have passed on.

What you will find is; generating revenue is easy with a smallish business. Generating revenue that exceeded expenses is more complicated problem. Many of the projects that people want you to quote are projects that don’t have money in them. Buyers put projects out to bid in search of the lowest bidder. A starving shop bites and begins spinning their wheels. Sad really. A budding entrepreneur won’t necessarily be able to see these projects for what they are until they have committed. The silver lining to this is that these experiences are the building blocks to the entrepreneurial mindset.

I still love the machine shop but I love it in a different way today. Had I had the opportunity out of college to run the shop I don’t know if I would have had the maturity to make it work. I was young and ignorant to so many business truths and human conditions. It took spinning our wheels a few times to show us there is work out there that is better left to our competition.

Accept That You Will Fail, Just Don’t Fail To Learn

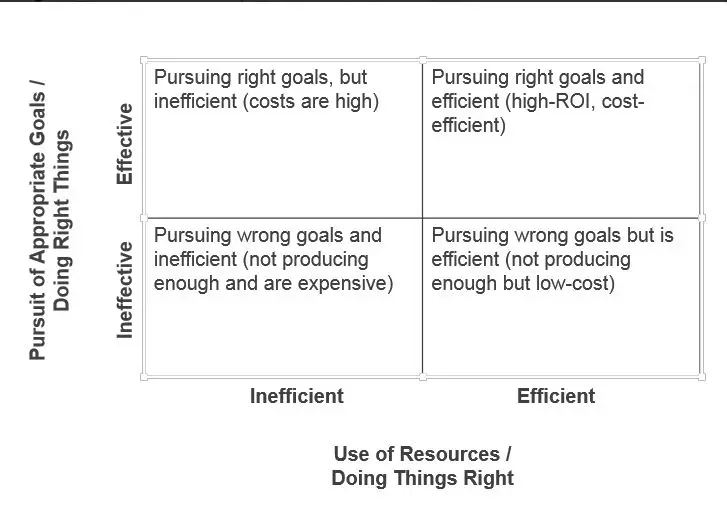

The one trait I have seen ring louder than almost any other with successful businesspersons is their ability to see through all the fluff. They don’t lean on forecasts, hope on promises, or blame things they can’t control. They are pragmatic to the core. They work off of hard figures, test their own assumptions, and distil all the noise around them down to fundamental truths. I wouldn’t say they are cynical, but they are certainly not going to bank on what other people tell them. Why do you think they are this way? The answer is because they have felt the pain and subsequent benefits of failure.

Having the humility and wisdom to understand when you screwed up is essential to conducting business well. I personally like the motto of; fail fast. There is more out there that you don’t know that what you do know. Accept this and don’t pretend to have all the answers. This advice is nothing new. Proverbs 16:16 ; How much better to get wisdom than gold, to get insight rather than silver. The value of knowledge and wisdom cannot be understated.

Entrepreneurs By Definition Don’t Follow The Crowd

To be an entrepreneur one must fundamentally be able to see opportunity and add value where others do not. This means the way you think aught not be consistent with the masses. You have an obligation to solve problems and provide solutions that others need. Others need you because they can’t take care of their pain the way you can. I find this rather exciting.

How cool is it that people need you? In what way is the world a better place because of what you do and how you do it? Your service to others will garner financial rewards but beyond the money I hope you can see the changes you are making!